FINANCIAL FAQs

HOW MUCH DO I QUALIFY FOR TO BUY A HOME?

A home is one of the most significant purchases you'll make, so knowing how much you qualify for when applying for a home loan is important. It is essential to be realistic about your monthly income and expenses. The general rule to follow is that your monthly mortgage payment should not exceed 28% of your monthly gross income.

The easiest way to learn what you may qualify for is to contact one of our licensed Mortgage Loan Originators. They can quickly calculate how much you may qualify for based on a few key numbers, including your income and any other earnings, estimated housing costs, down payment, current interest rates and more. You will also need a general idea of your monthly expenses. Keep track of all your expenses in a one-month period to come up with an average total for each month.

WHAT IS AN APR?

a. An annual percentage rate (APR) represents the average annual finance charge you’ll be paying on the loan when including all fees and costs associated with obtaining the loan. While the interest rate on a loan reflects the current cost of borrowing expressed as a percentage rate, the APR provides a more complete picture by taking the interest rate as a starting point and accounting for lender fees and other charges required to finance the loan.

b. Comparing APRs can help you understand how much you’ll be paying over the life of a loan. Factors that may affect the APR include:

-

- Points: These are discount points you can pay upfront to lower your monthly payments.

- Rates: The interest rate is a reflection of the cost you’ll pay to borrow the money. This could be a fixed-rate or an adjustable-rate.

- Fees: These can include processing and underwriting fees, settlement fees, appraisal fees, and more.

- Down payment: This is the amount you will pay upfront when you close your home loan.

- Private mortgage insurance (PMI): Mortgage insurance pays the lender a portion of the principal in the event you stop making mortgage payments.

I HAVE POOR CREDIT... CAN I STILL GET A MORTGAGE?

Some affordable lending programs allow homebuyers to obtain financing despite having previous credit issues, bankruptcies, and other financial concerns. You can work on your credit while allowing me to guide you on buying your first or next home. Different loan products may have more flexibility for homebuyers who have lower credit scores. An experienced Mortgage Loan Originator can help determine the loan to best fit your needs if your credit score is less-than-perfect.

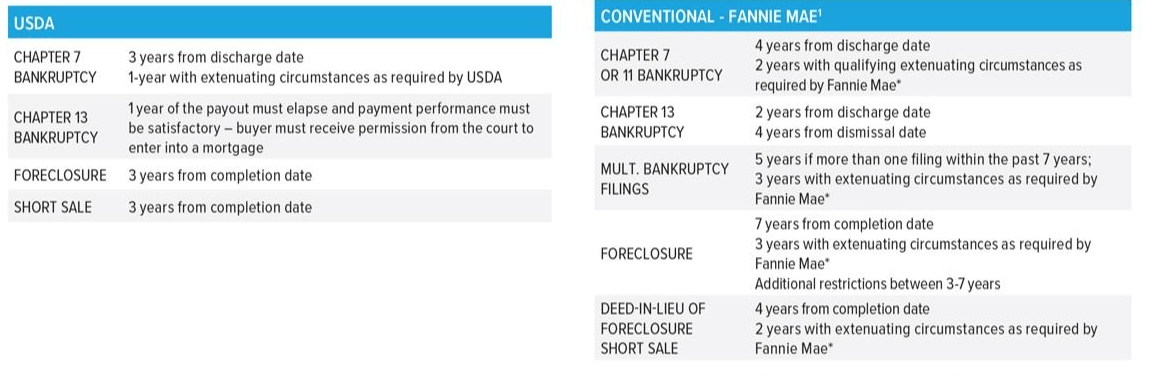

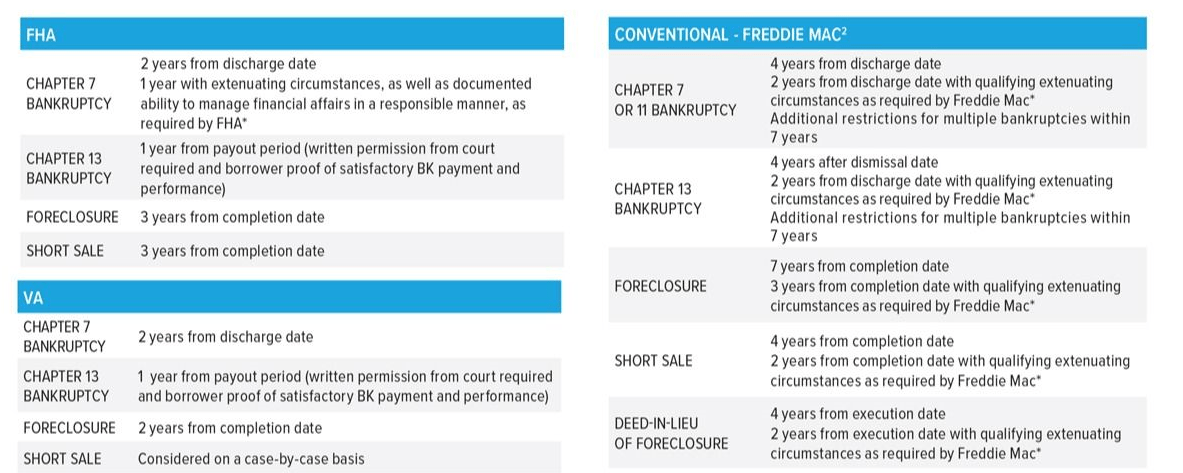

Obtaining a home loan after a bankruptcy is possible, although it may require a little patience. There is generally a waiting period before you can buy a new home, depending on the type of bankruptcy and the loan type you are seeking. Check out the chart below for more details and contact a Homebridge Mortgage Loan Originator to discuss your specific situation today.

* Information Courtesy of Homebridge Financial Services

|

|